.png)

Our efforts to close the gender investment gap

Summary

The last 12 months saw one of our best years ever in terms of investments made into female (co)founded companies. Our biggest challenge is top-of-pipeline: meeting more women founders pursuing businesses that match our mandate. And so while we didn’t quite make our target at the investment committee pitch stage, we are continuing our efforts, particularly at the top of the funnel this coming year.

Back in 2023, we first published our pipeline data and set a goal: for at least 40% of our investment committee (IC) pitches to be from teams with at least one female (or non-binary) founder.

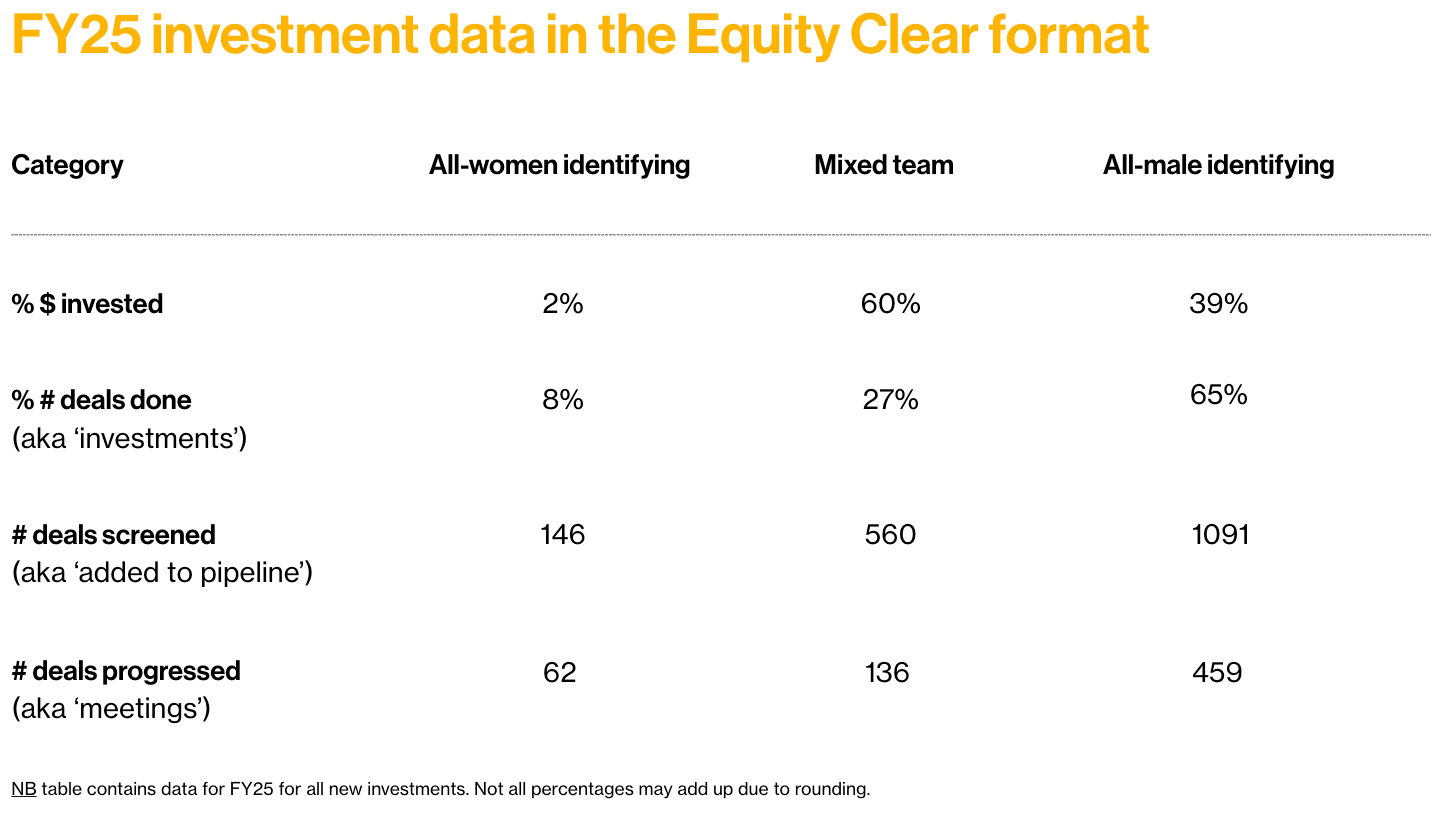

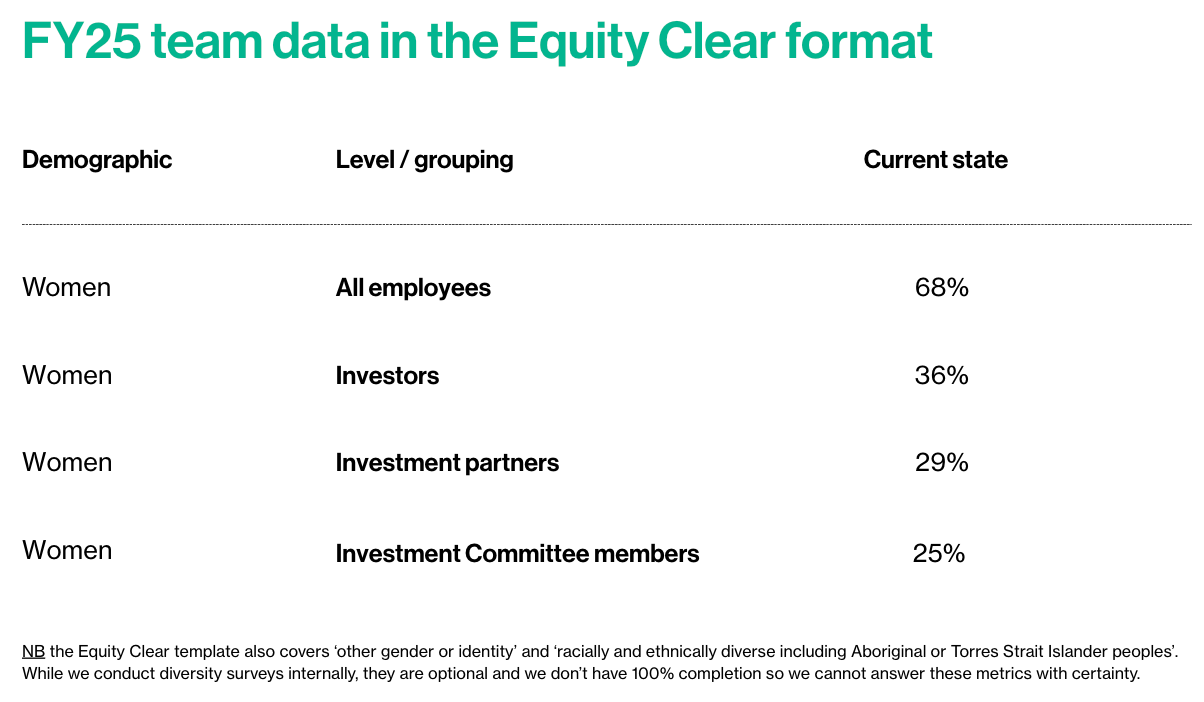

Since then, we have joined a group of other Australian and New Zealand VC firms publishing data in the new Equity Clear standard (our FY24 data is here).

How we did in FY25

We saw no change on our headline goal: 33% of the IC pitches were from teams with at least one woman. No change from FY23 and FY24. And, despite big efforts, our top of pipeline volume didn’t match the highs of FY24.

But, we saw improvement elsewhere in the pipeline, and in particular, capital investments.

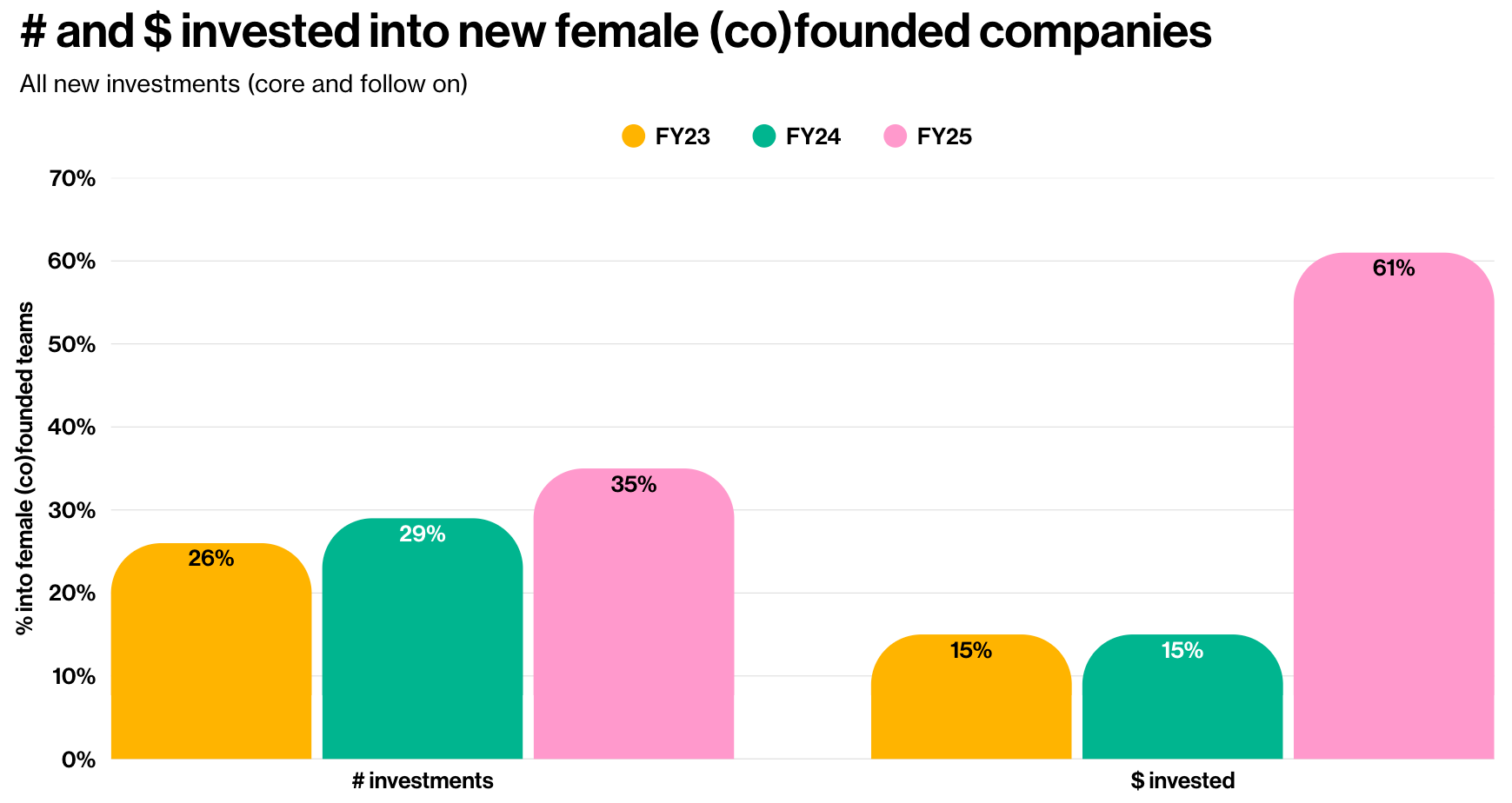

On a numbers basis, we had our busiest year yet. We made first bets on 9 new female (co)founded companies. That’s nearly twice FY24, and higher than any other year in Blackbird’s 12 year history.

That translated to 32% of the new investments out of our ‘core’ fund, or 35% of all new investments. Both up on previous years.

Another way of looking at this is that within 2 years, we’ve increased the share of our new investments into all-female and mixed teams by 9 percentage points.

In financial terms, those teams took about a quarter (24%) of the total dollars we invested into new companies from our core fund, or a whopping 61% if you include all new investments.

A note on terminology

We invest out of two types of funds:

- a ‘core’ fund: from which the majority of our new investments are made in pre-seed or seed rounds, and

- a ‘follow-on’ fund: which is where we invest bigger cheques in existing portfolio companies as they grow. In a rare set of cases, our first investment into a company is into a later round, and in those instances, the ‘follow on’ fund is deployed. That was the case for one company in FY23, one in FY24, and one in FY25 (Airwallex).

To keep things simple, from here on out, we’ll be reporting on all new investments made, regardless of whether it was the core or follow-on fund that first invested. To us, that’s the best indicator of how well we’re doing at bringing more gender diverse companies into our portfolio.

How does that compare to ‘the market’?

There’s no perfect measure of the ‘market’ for investible startups. But Cut Through Venture publishes the most comprehensive snapshot on the Australian market based on publicly available data.

With their help (thanks CTV!), we took a closer look at the last few years’ worth of data on deals done from pre-seed to Series B+, by gender make up of the founding team. That allowed us to compare our investing against a benchmark.

That analysis (shown below) told us that both we and the market have improved over the past three years. And that we’ve beaten the market in each of those years. It can feel painstaking at times, but progress is clearest at the macro level.

What have we learnt and what comes next?

Another way to understand progress is conversion.

We consistently invest in 1-2% of the companies that come into our pipeline. Our FY25 data has shown that female (co)founded companies are about as likely to succeed as their all-male counterparts. We’ve known for a while that female (co)founded teams that get to IC pitch tend to have a higher chance of getting a ‘yes’, but we’re now seeing that equalisation across the whole pipeline.

If we can maintain this, the challenge shifts even more clearly to sourcing: increasing the volume of women founders we meet in our investment mandate.

We spent FY25 experimenting with ideas in that space. Interestingly, these efforts didn’t translate to a higher volume of leads, but the improved conversion tells us something about getting better matches.

We hosted different types of events to maximise our chances of meeting women founding venture-scalable companies, or who might be inspired to do so.

We looked for ways to evolve the narrative away from just being a conversation about how little cash goes to women founders, to one that also showcases the impressive women who are already doing it.

And, finally, based on rich feedback from founders, we put more time behind demystifying the VC path so women who might be interested in it can make a decision about whether it’s right for them, and if so, how best to go about it.

That’s been the thinking behind the partnerships with content leaders like Missing Perspectives and Centennial World, as well as events with the likes of Michelle Battersby of Sunroom and the ANTI Network.

In FY26, we’re pouring even more energy behind these top-of-pipeline initiatives and adding new ones, including an exciting new collaboration with university VC firm NextGen to support their inaugural program, Verge, for women founders at uni. Perhaps unsurprisingly, the leaky pipeline starts early, and we’re keen to learn more about how to stem it, and support exceptional women who might want to pursue the founder path to get the access, support and resources they need.

On top of all this, as we mentioned last year, we’re continuing to see green shoots on the program side:

- Close to half (43%) of the teams that have come through our Giants program, for example, have at least one woman or non-binary founder in the founding team - and in FY25, 50% of the Giants companies that reached IC pitch stage did,

- 44% of the companies accepted into our Foundry program (for deep-tech university founders) have had a woman in the founding team, and

- Two-thirds (64%) of the participants in the Blackbird Foundation’s Protostars program identify as female or non-binary.

There’s a lot to be hopeful about.

If you’re building, or thinking about building, a company, we’d love to hear from you!

.avif)

.avif)